Japanese Yen (USD/JPY) Analysis

- Japan’s July trade balance likely impacted by a significantly stronger yen

- Economists and market participants expect another rate hike this year

- USD/JPY bearish continuation may receive a helping hand from the Fed

Japan’s July Trade Balance Likely Impacted by a Significantly Stronger Yen

Japan’s trade balance in July was worse than expected but the deficit was roughly half of what was seen in May and roughly one third of what it was in January. Imports in July rose more than anticipated while a stronger yen may have impacted exports, which were lower than expected.

The deficit has raised some doubts around the Japanese economic recovery, but trade balances have proven to be very inconsistent, typically rising one month and falling the next. After contracting 0.6% in Q1, the Japanese economy expanded by an impressive 0.8% in Q2 of this year, supporting recent measures from the Bank of Japan to raise interest rates to more normal levels.

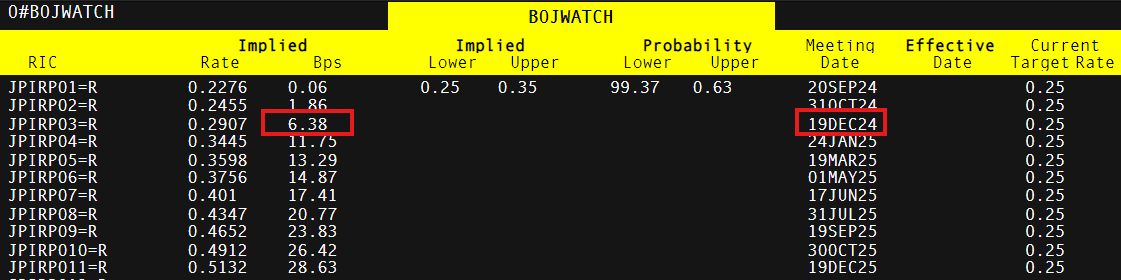

57% of economists polled by Reuters anticipate another interest rate hike in December this year. This comes off the back of two prior hikes, the most recent of which saw a surprise 15 basis points (bps) rise that caught many market participants off guard. Now, markets price in 6 bps heading into December but that is likely to hinge on whether the US can avoid fears of a possible recession which arose after the Fed voted against a rate cut in July, followed shortly by a worrying rise in the unemployment rate.

Richard Snow

Japanese Yen Eases after Sombre Trade Data

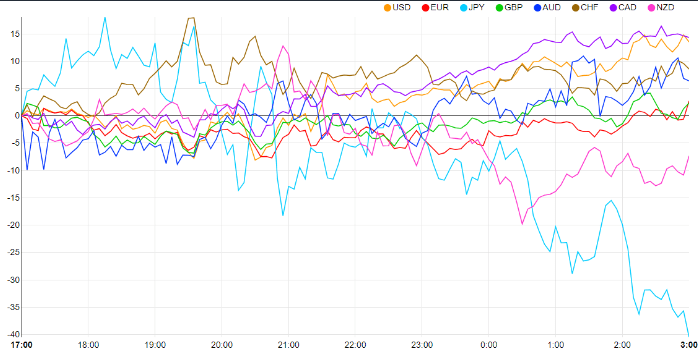

The Japanese yen headed lower in the early hours of trading, aided by the disappointing trade stats, with the Canadian and US dollars leading the pack for now. It won’t be surprising to see muted moves ahead of the FOMC minutes and an expected downward revision to job gains between April 2023 and March 2024.

The combination of lower inflation , rate cut expectations and a weaker jobs market have contributed to the steady dollar decline, which may very well continue if the FOMC minutes and job revisions paint a bearish picture. USD /JPY could therefore manage another leg lower after recently consolidating.

Richard Snow

USD/JPY Bearish Continuation May Receive a Helping Hand from the Fed

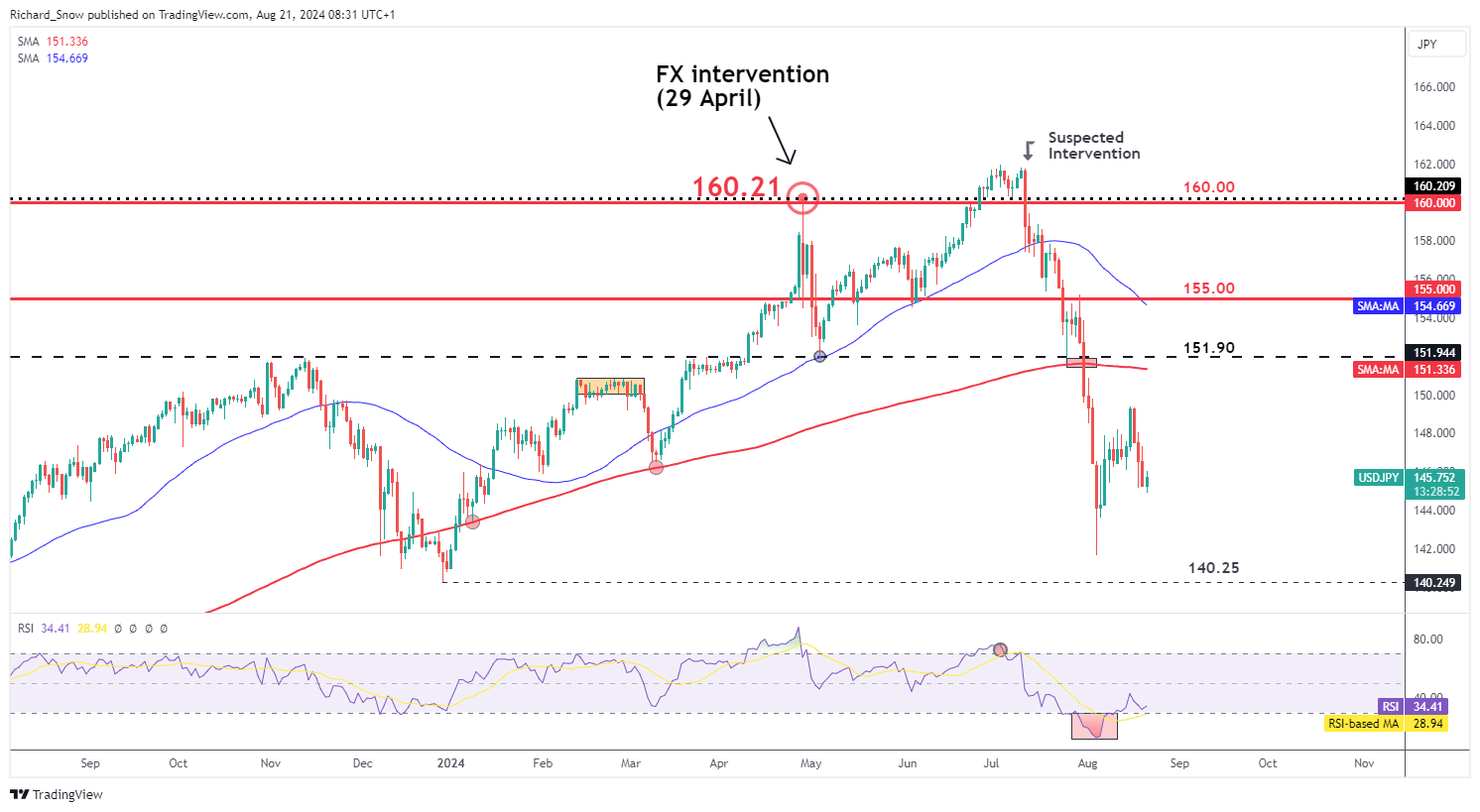

USD/JPY reached the swing low on Monday the 5th of August when volatility spiked as hedge funds rushed to cover carry trades. Since then, there has been a partial recovery as prices pulled back but ultimately, there has been a continuation of the more medium-term downtrend.

The US dollar has come under a lot of pressure as softer inflation and a worsening outlook in the jobs market has prompted traders to reduce USD exposure as the Fed prepare for the much-anticipated rate cut next month. This week’s Jackson Hole address from Jerome Powell will be followed with great interest. Speculation around a 25 bps or 50 bps cut continue to circulate, with markets assigning a 30% change the Fed will front load the rate cutting cycle.

The next level of support for USD/JPY lies at the spike low of 141.70, followed by the December 2023 low of 140.25. With some time to go until the BoJ is expected to hike, the catalyst of a further bearish move in USD/JPY is more likely to come from the US with the FOMC minutes, jobs revision, and Jackson Hole Economic Symposium all taking place this week. Resistance appears at the recent high at 149.40, followed by the 200-day simple moving average (red line) and 151.90 level.

Richard Snow