US Crude Oil Prices, Analysis and Chart

- US Crude remains just below the $80 mark

- This week has seen its range top survive a challenge

- OPEC Plus is expected to extend current production cuts on Sunday

Crude Oil Prices were a little lower in Europe on Thursday, retracing some more of the gains made earlier in the week. Those gains were rooted in hopes that the Organization of Petroleum Exporting Countries and their allies will stick with current, voluntary production cuts at their policy meeting on Sunday. The impending start of the summer ‘driving season’ in the United States has also boosted hopes for increased gasoline demand.

Figures from the American Petroleum Institute showed that crude stockpiles were down by 6.59 million barrels in the week ending May 24. Focus now shifts to the Energy Information Administration’s inventory snapshot. That’s coming up later on Thursday.

Israel’s strikes on the Palestinian city of Rafah have also kept conflict in the Middle East unfortunately to the fore, with the US West Texas Intermediate oil benchmark and the global Brent market up by more than 1% this week.

Still, despite plenty of fundamental support, the energy market like all others remains uncertain as to when interest rates could start to fall in the US and, when they do, how many reductions there might be. While the economic resilience that keeps rates high is not necessarily bad news for oil demand, oil bulls are always happier when central banks are in stimulus mode.

Futures markets think September is the most likely time for US interest rates to start falling, and that they might just come down sooner in Europe. But these forecasts remain subject to the inflation data, which means those numbers are important to all markets. The next major example is the US Personal Income and Expenditure series which is coming up on Friday.

After that it will be ‘over to OPEC.’

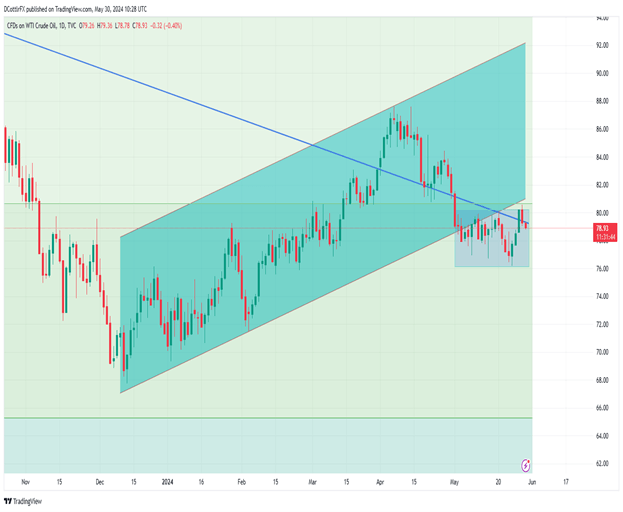

US Crude Oil Technical Analysis

WTI Crude Daily Chart Compiled Using TradingView

Having broken below their previously dominant uptrend channel from mid-December back at the start of May, prices have essentially continued to trade sideways since, within a rather narrow range between $80.18 and $76.23/barrel, the latter being a two-month low. Note, however, that even those levels have been tested infrequently and that the usual trading range has been even narrower than that.

This week’s trade saw bulls try to push past the range top on Tuesday, but they couldn’t manage it and the month looks set to close out with that established band still in place. That makes a lot of sense given the high degree of fundamental uncertainty over demand and monetary prospects.

The market is now hovering around support from its long-term downtrend line from June 22, which now comes in at $79.35, with resistance at the retracement level of $80.68.

Oil - US Crude

Bullish

of clients are

net long.

of clients are

net short.

| Change in | Longs | Shorts | OI |

| Daily | -12% | -2% | -10% |

| Weekly | 10% | 17% | 11% |