One of the most valuable lessons on building wealth was taught to me by my father at a very early age. My dad was always a very hard worker. But what he emphasized in his personal life was the discipline of saving. What Dad taught was that the first step to building wealth is learning to live well below your means. While this idea sounds like it is common sense, I revisit it regularly in my personal financial life to make sure I don’t forget it.

The importance of living well below your means is at odds with our consumption-based society. Dad taught that by living well below his means he would save money and invest the difference in investments that could greatly multiply his wealth. Savings are the foundation of wealth building because it represents deferred consumption, allowing individuals to accumulate capital that can be invested for future growth. By setting aside a portion of income rather than spending it, people can create a financial buffer, seize opportunities for investment, and compound their returns over time. Savings not only provide security but also open the door to wealth-building strategies such as purchasing assets, starting a business, or investing in the stock market. Without the discipline of saving, it becomes difficult to leverage opportunities and grow wealth over the long term.

The alternative to this perspective is the temptation to consume and to do so on credit. In contrast, today’s consumption-based society encourages immediate gratification through credit, creating a cycle of debt rather than wealth. When people consume on credit, they trade future income for present desires, often paying higher costs through interest and fees. This model promotes a culture of living beyond one’s means, where debt becomes the norm and the focus shifts from building wealth to sustaining consumption. As credit becomes more accessible, many individuals fall into a pattern of financing lifestyles instead of investing in long-term financial health. This consumption-driven mindset hampers wealth accumulation and makes financial independence more difficult to achieve.

The stark contrast between savings and credit highlights a harsh reality: while savings are the key to long-term wealth and financial independence, our society is structured around debt and consumption. As we navigate the current presidential election cycle, it’s clear that neither political party prioritizes your desire or ability to save money. Both sides, instead, promote policies aimed at stimulating consumption through easy credit, government spending, and promises of economic growth driven by more debt. Encouraging savings would require a fundamental shift in our economic system, one that places emphasis on financial discipline and delayed gratification—concepts that are at odds with the consumption-driven economy in which we live. The focus remains on short-term spending, not long-term savings, leaving individuals trapped in a system where accumulating wealth through disciplined savings becomes increasingly difficult.

The greatest concern that I witness and experience on a regular basis regarding inflation and the dollar debasement policies which we are experiencing is that it is becoming harder and harder to save. If the government does not encourage saving, I must conclude that they are equally at odds with my wealth creation efforts.

Longtime readers of this blog recognize that I consider most of the government economic reporting to be gaslighting and propaganda. The entire field of economics at the governmental level is monopolized by Keynesian economists who operate under the perspective that debt and government spending are the recipe for a long-term healthy economy. The myth that is created from this belief system is that you can solve all problems by simply creating more debt. The belief that debt is the lifeblood of a healthy economy is a dangerous misconception that has led to the perpetual cycle of borrowing we see today. This flawed perspective fosters the idea that any debt problem can be resolved simply by creating more debt, an approach that has been embedded in our economic system since the Federal Reserve Act of 1913. Under this framework, debt is seen as a tool for growth, with borrowing encouraged at every level—from individuals to corporations and governments. However, this reliance on debt masks deeper structural issues, as it creates only temporary solutions while deferring financial reckoning. Instead of fostering true wealth and stability, the economy becomes more fragile, dependent on the constant expansion of credit, and vulnerable to crises. The underlying assumption—that more debt can solve the problems created by too much debt—has kept us on an unsustainable path, with long-term consequences for financial security and economic health.

Yesterday the Consumer Price Index was released to mixed reviews. The latest Consumer Price Index (CPI) report, released on September 11, 2024, showed a year-over-year inflation rate of 2.5%, down from the previous month’s 2.9%. This marks a continued easing of inflation, largely driven by stable food prices and falling energy costs. However, core CPI—which excludes food and energy—showed a slight acceleration, which raised concerns that inflation may not be cooling as fast as hoped. Housing, specifically rent and owner’s equivalent rent, remained a significant driver of inflation, which is concerning since it makes up about 40% of the core CPI.

My issue with the report is that it bears absolutely no resemblance to economic reality for anyone in the economy. I consider it to be financial propaganda of the highest order.

I know this sounds extreme to most. But when you watch the Fed and government economic reports for as long as I have you will come to appreciate that “economic truth” in no way resembles anything reported by government agencies. Economic propaganda has increasingly become a powerful tool in shaping perceptions, especially for traders and investors who rely on clear, accurate data to make informed decisions. When the narrative around economic figures is manipulated—whether it’s inflation, employment, or GDP—interpreting the reality becomes a challenge. The analogy, “if it walks like a duck, quacks like a duck, and looks like a duck, but the government calls it a raccoon,” highlights this issue. Investors are left questioning whether the economic data they’re given truly reflects reality or if it’s being redefined to suit a political or institutional agenda. This manipulation fosters confusion and erodes trust, making it difficult to decipher actual market conditions from what is being portrayed. In this environment, traders must navigate a sea of misinformation, further complicating their ability to make accurate market predictions.

The following two graphics are links to recent economic reporting which I consider to be highly suspect, to say the least.

The recent adjustment by the National Bureau of Economic Research (NBER) to remove 818,000 jobs from previously reported employment data is a significant development that ripples through numerous key economic indicators. Employment figures are critical to understanding the broader economy, and when so many jobs are retroactively removed, it calls into question the accuracy of prior estimates on real income, consumer spending, sales, productivity, and even Gross Domestic Product (GDP). Each of these metrics relies on employment data as a key input; if the jobs numbers were inflated, then assumptions about consumer spending power, economic output, and overall economic health were likely skewed. Without accurate jobs data, it becomes nearly impossible for analysts and investors to assess the true state of the economy.

To provide a sense of scale, let’s hypothesize that each of these 818,000 jobs paid an average salary of $50,000 per year. This translates to over $40 billion in annual income that was previously thought to exist but does not. When annualized, this missing income adds up to $40.9 billion, representing a massive shortfall in what economists previously assumed was flowing through the economy. This not only impacts household income data but also reflects poorly on estimates of real consumer spending, a major driver of GDP. Furthermore, with 818,000 fewer jobs, productivity metrics are overstated, as fewer workers producing a similar level of output would have artificially boosted productivity figures.

The reality is that $40.9 billion is a colossal amount of money for most states and economic sectors, but in Washington, D.C., this figure may be seen as insignificant or inconsequential. Federal budgets and deficits regularly reach into the trillions, and massive sums get lost in bureaucratic inefficiencies or political rhetoric. However, to the broader economy and especially to individuals, $40.9 billion represents real wages, real consumer spending, and tangible economic impact. It is a stark reminder of how out of touch Washington D.C. can be when discussing fiscal policy, often underestimating the importance of such figures for the real economy and everyday Americans.

I was recently listening to a podcast where economist Dr. Lacy Hunt was being interviewed about the 818,000 jobs being removed from the economic data. Dr. Lacy Hunt is a heavyweight in the world of economics, with decades of hard-earned experience dissecting macroeconomic trends and navigating the complexities of monetary policy. As the Executive Vice President of Hoisington Investment Management, he’s been a key figure, offering sharp insights into interest rates, inflation, and the long-term shifts that drive the economy. Before taking on this role, Dr. Hunt held senior positions at the Federal Reserve Bank of Dallas and the U.S. Treasury, adding to his deep bench of expertise.

His real focus, though, lies in understanding how high levels of debt weigh down economic growth. He’s been a vocal advocate for policies that prioritize long-term economic stability over the short-term sugar highs of government stimulus. Dr. Hunt has built a reputation warning against the dangers of excessive debt, regularly speaking and writing on deflationary risks. Within financial circles, he’s earned deep respect, standing as a leading authority on how debt and monetary policy shape the economy’s future. Dr. Hunt referred to the removal of 818,000 jobs from the jobs roles as a “5-sigma event.”

A “5 sigma event” refers to an occurrence that deviates from the mean (average) by five standard deviations (σ) in a normal distribution. In terms of probabilities, such an event is extremely rare. The probability of a 5-sigma event happening in a normal distribution is about 1 in 3.5 million, or 0.000057% . This means that such events are far outside what is expected under normal conditions, often indicating a highly unusual or outlier occurrence. In finance, for example, a 5-sigma event typically signals something extraordinary, beyond normal fluctuations or random chance. To provide perspective on what this means, a “5 sigma event” in blackjack would be like hitting blackjack (an Ace and a 10-value card) 21 multiple times in a row. The chances of getting blackjack in a single hand are about 4.83%. To have a string of blackjacks that compares to a 5-sigma event, you’d need to get about 21 blackjacks in a row.

That’s because the probability of hitting 21 consecutive blackjacks is roughly as rare as a 5-sigma event in statistics, which has a probability of around 0.000057%, or 1 in 3.5 million. So, if you ever got 21 blackjacks in a row, it would be an occurrence as rare as a 5-sigma event, something that hardly ever happens!

The reason I share this bit of information with you is that when a 5-sigma event occurs it is either incredible fortune or outright fraud. There cannot be a middle ground.

I can assure you that if you or I walked into a casino and received 21 blackjacks in a row, chances are extremely high that we and the dealer would immediately be subjected to a vicious police interrogation which would be rightfully deserved. The fact, that this has not occurred with the jobs numbers and the National Bureau of Economic Research tells me that the dark underbelly of economic reporting is a shadowy realm where the truth is twisted and dressed up to fit a narrative, often endorsed by the very authorities who are supposed to protect the public interest. It’s a place where inconvenient data gets buried, revisions go unnoticed, and rosy projections are pushed, all while underlying problems like debt, inflation, or wage stagnation are glossed over or downplayed. This creates a false sense of economic security, masking the reality faced by businesses and individuals. It’s the kind of propaganda that keeps investors and the public chasing illusions, all while the foundational cracks in the economy widen. When those in power knowingly push these narratives, it becomes a dangerous game, leaving traders and investors to decipher a reality that’s purposely obscured by those pulling the strings.

Why is this important? Whether you are a trader or an investor, you have a choice, you can believe in Math or Central Banking.

Let me explain.

One of my canary in the coal mine indicators that I have discussed numerous times over the past few years is to simply look at the comparison of gold performance versus the S&P 500 indicators over multiple time frames. My observation is when Gold outperforms the broader stock market, things get very weird in financial reporting.

While I do not like the conclusions, I do try and exhaust all other possibilities before I commit myself to a perspective. The reason I consider this performance grid important is because Gold is considered anti-Wall Street. It is an inflation hedge and an insurance policy against currency debasement. Gold is trailing on a 5-year and ten-year basis, but it is maintaining a solid lead on all other important time frames.

While I can only speculate what this might mean, I can conclude that Gold is tuning in on some of the financial issues in the world economy which center around debt and currency debasement which is occurring globally.

Next, one of the news stories that has troubled investors over the past two months is that Warren Buffett reported that he was moving heavily into cash and T-bills. Why would the Oracle of Omaha move mostly into cash?

Warren Buffett has earned his reputation as one of the greatest investors in history due to his consistent, long-term outperformance in the stock market. The nickname “Oracle of Omaha” comes from his ability to predict market trends and his deep understanding of business fundamentals, which have guided him to extraordinary success. Buffett’s investment philosophy, focused on value investing, long-term growth, and disciplined capital allocation, has been central to his success.

From 1965 to 2023, Berkshire Hathaway delivered an average annual return of about 20% compared to the 10% annualized return of the S&P 500 during the same period. This performance has led to an overall gain of more than 3.7 million percent, far exceeding the market’s growth.

If you had invested $1,000 with Warren Buffett in 1970, your investment would have grown dramatically due to Berkshire Hathaway’s compounding returns. Since Berkshire has delivered an average annual return of about 20% over more than five decades, your $1,000 investment would likely be worth over $10 million today.

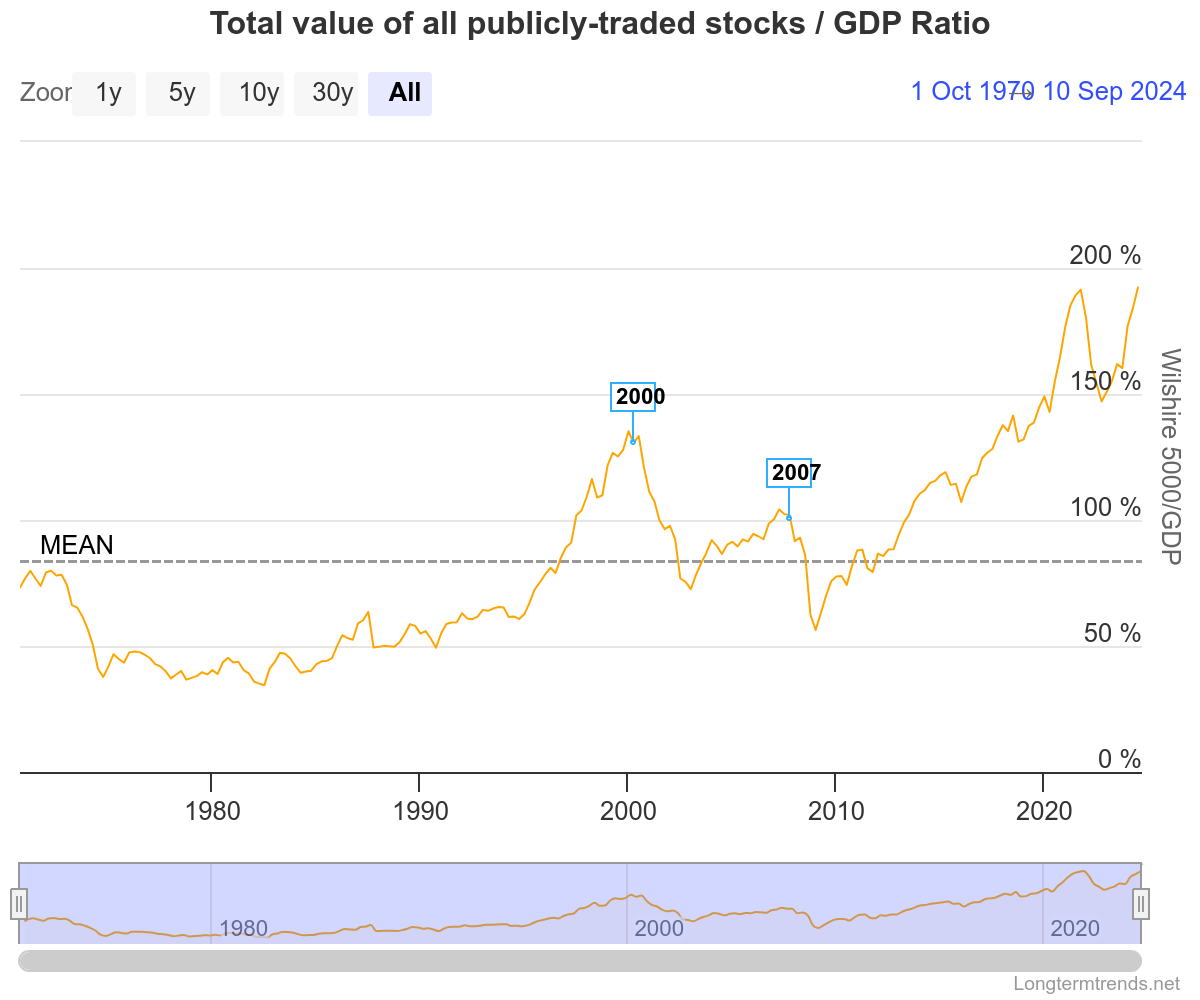

Check out the Valuation of the Warren Buffett Indicator which is a metric which is the market capitalization of all stocks in comparison to the GDP. It is the most overvalued stock market in history.

LongTermTrends

My conviction is that Mr. Buffett is simply stating the obvious, you can believe in Math and historic valuations or Central Banking. His conclusion is that valuations will win in the long run.

False economic numbers create significant distortions in markets because they obscure the true state of the economy, leaving traders and investors guessing. When the data being relied upon is inaccurate or misleading, it becomes difficult to gauge market valuations, assess risk, or anticipate future trends. This is especially crucial in the current environment, where extreme stock market valuations, such as those highlighted by Buffett’s stock market cap to gross domestic product metric, point toward a potential correction. Meanwhile, the Federal Reserve’s decision to cut rates despite high valuations suggests an underlying economic weakness that has not been fully acknowledged. Investors are now forced to choose between trusting central bank policies or relying on mathematical models that signal the possibility of significant market losses. Historical market performance shows that severe pullbacks often follow periods of overvaluation, and current conditions indicate the S&P 500 may face a steep decline to return to more sustainable levels. Adding to this complexity is the psychological wealth effect, where inflated asset prices make some individuals feel wealthier, though these gains are disproportionately enjoyed by a small group, sparking political discussions about taxing unrealized gains.

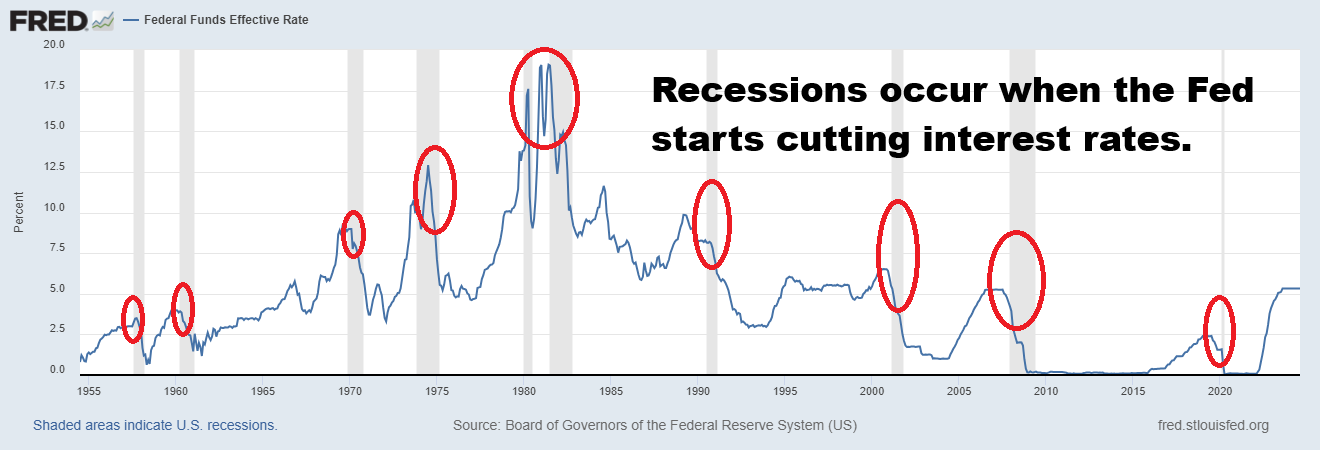

Lastly, let me draw your attention to what happens historically when the Fed lowers interest rates.

The economic reality is that the Federal Reserve does not lower interest rates when the economy is performing well; instead, it typically cuts rates when the economy is struggling. Lowering interest rates is a traditional tool used by the Fed to stimulate economic activity by making borrowing cheaper for businesses and consumers . When rates are reduced, companies can access capital more easily, encouraging investments in growth, expansion, and hiring, while consumers benefit from lower loan and mortgage costs, driving increased spending. This boost in economic activity is intended to counteract slowdowns, recessions, or periods of financial distress. However, when the Fed lowers rates despite high market valuations or seemingly strong growth, it can signal underlying economic weaknesses that aren’t immediately visible in headline indicators.

In contrast study the news story that Treasury Secretary Janet Yellen is promoting claiming the economy is strong and resilient, and we are headed for a soft landing.

Please keep in mind this is the same Janet Yellen that told you that inflation was transitory.

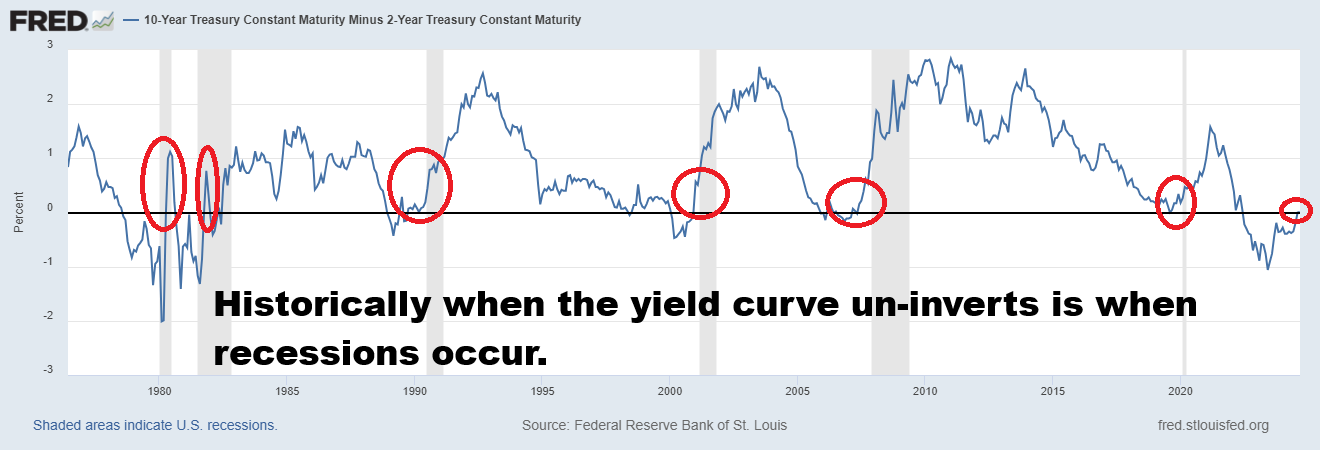

But let’s look at the yield curve historically again and not pay attention to what the financial media or monetary authorities are promoting. Below is the chart of the Yield curve going back 45 years. Notice how the yield curve un-inverts is when the recession fireworks occur?

For traders and investors, understanding these dynamics is crucial. Staying overly aggressive in equities amid these overvaluations could be disastrous, especially as bubbles—such as the current A.I-driven stock surge led by companies like Nvidia—could burst, triggering widespread market declines. Managing inflation and wealth is equally challenging, as inflation continues to erode purchasing power despite investments, making it essential for investors to focus on strategic asset allocation and long-term planning. Moreover, looming uncertainties around tax policy, particularly the possibility of higher capital gains taxes or taxes on unrealized gains, add further layers of risk. In this highly volatile and uncertain environment, investors must stay cautious, potentially positioning themselves in short-term instruments like Treasury bills or safer assets like gold and silver, while remaining vigilant about the broader economic and market conditions.

We are in an election cycle. Everything in the financial news is oriented around this event. The incumbent administration always wants to make the economy look better than it is. The challenger will always proclaim that it is worse. As traders we want to know the truth and concern ourselves whether that matters.

Our duty as traders is to recognize that neither side of the aisle is going to do anything to stop the currency debasement which makes it almost impossible for people to save. The proposals generated by Republicans and Democrats are laughable if they do not address the persistent debasement of our currency. The reason I am stating this is that you can’t solve a debt problem by creating more debt.

Last week the Republicans announced that Elon Musk would be head a commission to stop government waste. Do you remember the Grace Commission was formed in the 1980s by President Ronald Reagan to investigate waste and inefficiency in the federal government? It recommended ways to reduce government spending. The commission’s report found significant areas of waste but concluded that even if its recommendations were fully implemented, it would not eliminate the federal budget deficit due to the continued growth of entitlement programs and interest on debt. At the time, annual budget deficits were averaging around $100 billion per year, contributing to rising national debt concerns. The Grace Commission played well to the Republican base in the 1980’s and that was $34 trillion dollars ago as far as the National Debt goes.

On the Democratic Side of the aisle equally ridiculous policies are being floated around regarding price controls. The implementation of price controls in the 1970s, particularly under President Nixon’s administration, was an attempt to curb rising inflation by capping prices on goods and services. While the intention was to stabilize the economy, the results were disastrous. Artificially limiting prices led to widespread shortages as producers, unable to cover rising costs, cut back on production. This created supply chain disruptions, long lines for basic goods, and black markets, as the natural balance between supply and demand was distorted. Instead of controlling inflation, price controls exacerbated economic instability, leading to stagflation—a combination of stagnant growth and high inflation—that plagued the U.S. economy throughout much of the decade.

The reason I am making these harsh comments is because regardless of who your political knight in shining armor is, it is still your responsibility to protect yourself from the monetary printing press which is guaranteed to run 24/7 in the weeks/months and years ahead. When I assess the current economic landscape, it’s clear to me that the dollar must be devalued to keep the system afloat. Wars need funding, and the ever-growing debt requires constant refinancing. On top of that, it’s an election year, which means we’re bombarded with promises of “free” benefits if we choose the right politicians. All of these factors contribute to rising asset prices when measured in U.S. dollars.

Number go up because the value of the currency goes down. Rising asset prices do not mean the underlying economy is doing well. Today, rising asset prices are occurring because currency debasement is how the government pays back the $25 trillion debt.

As a trader you need to decide, do you bet on Central Banks or on historical valuations of normal?

My suggestion is that to assist you in protecting your wealth that you learn how to trade with artificial intelligence.

What’s your best shot at making serious money in today’s financial markets?

The answer A.I. gives will blow your mind.

Right now, Artificial Intelligence, Machine Learning, and Neural Networks aren’t just fancy buzzwords—they’re your lifeline for protecting and growing your portfolio.

Let me be crystal clear: I have a rock-solid belief that if the Fed sticks to its plan, stocks are going to tank. But here’s the thing… my NORTH STAR isn’t my gut—it’s the trend, and A.I. is the only tool sharp enough to find it, follow it, and make it pay.

A.I. combined with neural networks gives you the analytical firepower you need to ride the right trend at the right time. Nothing else comes close.

Here’s the deal: If you can’t handle the brutal reality of a zero-sum game, step aside. The markets are survival of the fittest. But here’s the beauty of A.I.—it learns from every misstep, remembers every failure, and relentlessly pursues the next winning move. That Feedback Loop is the secret weapon of every successful trader I know.

And that’s where the real money is made.

While the talking heads babble about economic theory, my only allegiance is to the trend. With VantagePoint artificial intelligence in your corner, you don’t need theories—you need profits. And A.I. delivers that, day in and day out.

Ready to get serious? Let’s follow the trend and make some money.

Visit With US and check out the a.i. at our Next Live Training.

PAY ATTENTION!

It’s not magic. It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.